Dec 8, 2025 // Dr. Stephan LemkensFrom Biometrics to AI Agents: 7 Banking Trends for 2026Seven tech and regulatory trends European banks and PSPs must prepare for in 2026

Nov 18, 2025 // Dr. Stephan LemkensWhen Speed Becomes a Compliance Issue: How AML Processes Are ChangingToday, it no longer matters whether banks can detect suspicious activities. Instead, what matters is how quickly and consistently the downstream processes function. This is precisely where the focus of supervision lies.

Nov 4, 2025 // Christian HueschWhat Links Alfred Hitchcock to Fraud and PSD3?Like a Hitchcock thriller, PSD3 brings suspense to Europe’s payments. Discover how RiskShield turns regulatory tension into fraud-prevention readiness.

Oct 12, 2025 // Tyrone CastelanelliAI, Trust & the Digital Euro: SIBOS 2025 InsightsDiscover our key insights from SIBOS 2025 in Frankfurt: how AI, trust, and the digital currencies are shaping the future of global finance.

Aug 18, 2025 // Dr. Stephan LemkensTackling Today’s AML Challenges: Expert Insights that MatterWhat are the biggest challenges in AML today – and how can compliance teams respond effectively? In this expert interview, we explore five critical questions, from smarter alert handling to seamless audit readiness and strategic resource scaling.

Jul 14, 2025 // Katrin SchlüterFRAML Blog – Rewards, Risks, and Realities of IntegrationFRAML is more than just a buzzword: it’s a shift in how financial institutions approach fraud and AML. This blog unpacks what’s driving the trend, where the risks lie, and how it can be made to work in practice.

May 21, 2025 // Hannah KuckFrom Vision to Obligation: Banks and PSPs on the Road to Instant Payment The new EU regulation makes SEPA Instant Payments mandatory from 2025. The countdown to implementation is now beginning for banks and payment service providers. What is required by regulation - and how fraud risks can be managed in real time.

May 12, 2025 // Martin BradleyThe Fight Against Scams: How Intelligent Dynamic Profiling Changes the GameFinancial institutions face an alarming rise in sophisticated scams and account takeover attempts.

Apr 29, 2025 // Hannah KuckInstant Payments and Risk Management: Three Actors Caught Between Regulation and Real-Time Pressure Instant payments demand real-time fraud prevention - how can risk, compliance, and sanction experts keep up with the pressure and regulation?

Oct 29, 2024 // Hannah KuckEvent Review: 9th International RiskShield Networking EventIn 2024, INFORM's RiskShield Networking Event once again brought together customers, industry experts and others to talk about combating financial crime.

Apr 23, 2024 // Halyna HermannsEvent Review: 13th Digital Banking and Mobile Payments SummitExplore our event review for insights from the 13th Digital Banking Summit in Vienna, featuring RiskShield's profound expertise in digital risk management.

Mar 15, 2023 // Tyrone CastelanelliInterview on how to effectivly and efficiently fight Money LaunderingRoy Prayikulam, Senior Vice President Risk & Fraud at INFORM provides an overview. At INFORM, he is responsible for fighting financial crime with the help of Hybrid AI and algorithms.

Oct 27, 2022 // Tyrone CastelanelliEvent Review: Networking at its BestAt the end of September 2022, the INFORM Risk & Fraud Department invited its customers and partners to its 7th International RiskShield Networking Event.

May 3, 2022 // Roy PrayikulamInnovations in Payment Fraud – And How to Stay Ahead of Them2021 was a year of innovations in payments, from the wider acceptance of blockchain and cryptocurrency to new forms of digital wallets and currency.

Oct 11, 2021 // Andrea Vieten8 Proven Success Factors for the Implementation of Modern Decision-Making SoftwareQuestion: What do process optimization, monitoring of transactions and non-financial events, risk-based authentication, fraud prevention, list screening, and probability analysis for high costs have in common?

Sep 14, 2021 // Roy PrayikulamUsing Artificial Intelligence in the Fight Against Money Laundering and Terrorist FinancingThe European Financial Supervisory Authority estimates that transactions involving "dirty" money now account for around 1.5% of annual gross domestic product in the EU - that's 133 billion euros. The European Union therefore wants to block a larger portion of these dirty deals and has its sights set on a new directive this fall.

Jun 17, 2021 // Roy PrayikulamPSD2 Made Strong Customer Authentication Mandatory – Risk Based Authentication Makes it ConvenientStrong Customer Authentication (SCA) is designed to protect banks and customers from fraudulent activity, but it creates high overhead costs and can compromise customer convenience and revenue opportunities. Using risk-based authentication (RBA) can mitigate these hurdles without sacrificing transaction security.

Feb 23, 2021 // Roy Prayikulam5 Things a PSD2-Compliant Fraud Prevention Software Must Be Able to DoBanks and payment service providers have had two major challenges thrust their way because of the COVID-19 pandemic. Firstly, there is a boom in online commerce which is leading to a flood of payment transactions and their accompanying fraud attempts.

Feb 25, 2020 // Roy PrayikulamFighting Financial Crime with Hybrid AIMachine learning is nothing new. In fact, many of the algorithms used to make predictions have been around for decades. Nevertheless, there is a current hype around the topic of Artificial Intelligence and Machine Learning that spans across nearly every industry, and banking is no exception.

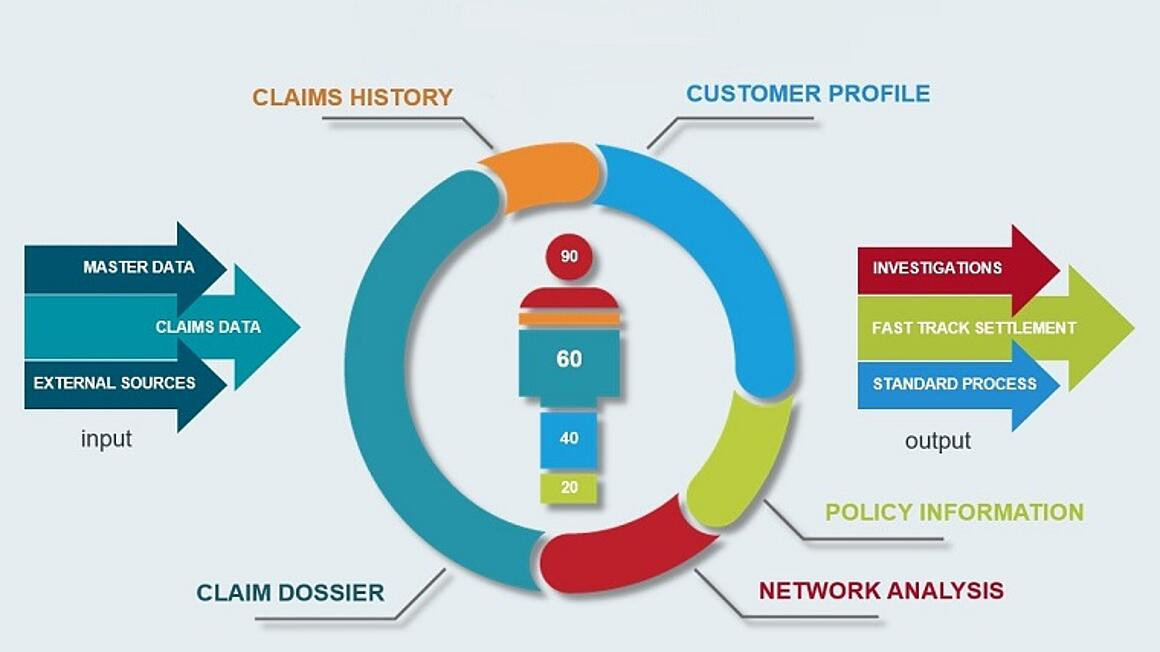

May 15, 2019 // David Weaver3 Tips for Deterring Insurance FraudI will never forget my first car accident. I was 16 and had just completed the roundtrip journey from San Jose to Santa Cruz over Highway 17 in California; a tough drive for a beginner, through the winding mountain roads.

Apr 2, 2019 // Halyna HermannsHow To Detect Terrorist Financing Using Artificial IntelligenceAt the same time, banks and payment service providers have to optimize business processes, control their costs and manage human resources to handle the fast-growing volumes of digital payments on a day-to-day basis.